Salvaging a meaningful carbon market price in Alberta

Doable but improbable as MOU negotiations continue

Alberta and Canada claim to be making good progress on a carbon pricing deal after missing their self-imposed April 1st deadline, needing only to resolve how fast the province will ramp up to the previously agreed $130/tonne effective carbon price.

This is a bit like saying they’re very close to having a baked cake needing only to buy ingredients, mix them together, and put it in the oven for a while.

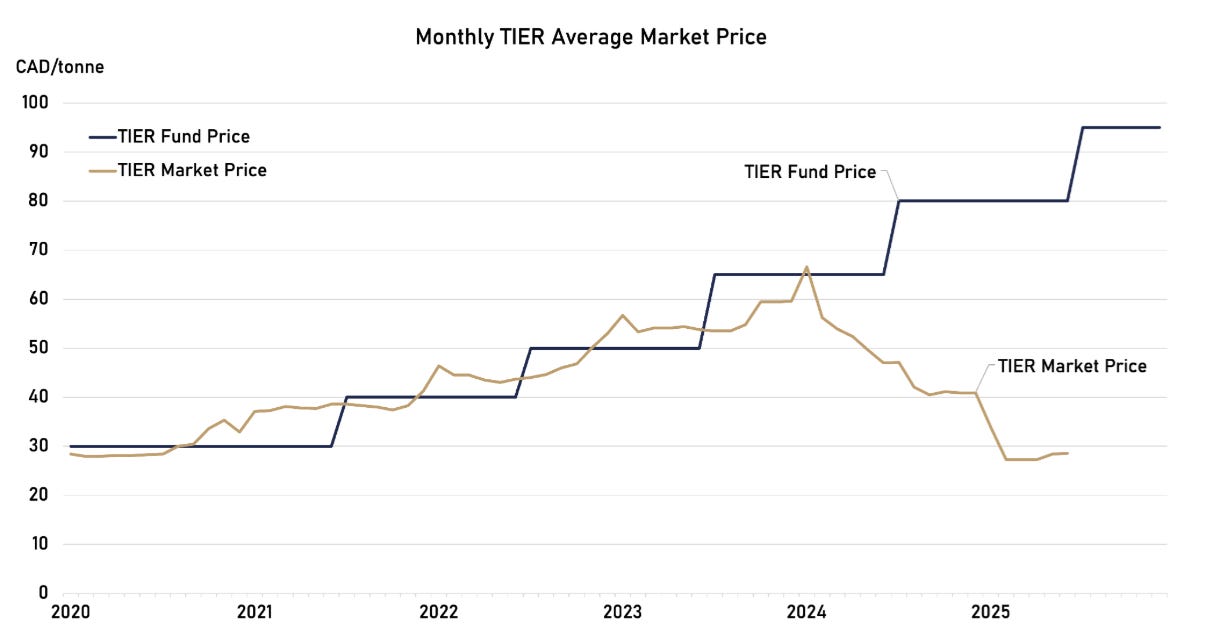

Alberta’s regulated carbon price was $95/tonne last year while the effective market price hovered around $20/tonne. The regulated price could be moved to $130/tonne tomorrow but unless market structure issues are addressed, the effective market price would continue to languish. Moving that price upward is the entire issue under negotiation.

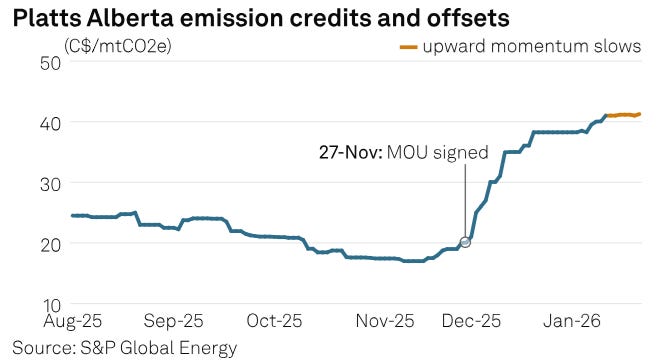

The Memorandum of Understanding Alberta and the Feds signed in November included planned investments in data centres, pipelines, and Carbon Capture and Storage (CCS) projects – none of which can advance until this carbon pricing agreement is complete. The market problem is solvable but the two governments have not been close on this topic in nearly a decade.

Undermining the market

Alberta’s United Conservative Party (UCP) first took power in 2019. It almost immediately went to work relaxing compliance rules under the province’s Technology Innovation and Emission Reduction (TIER) program.

TIER

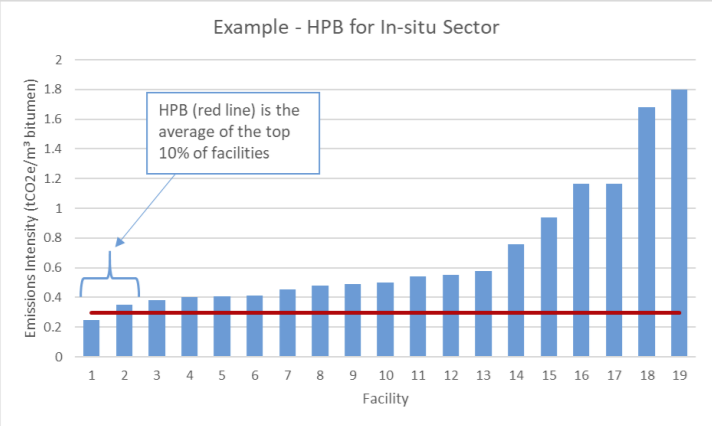

The Alberta NDP adopted TIER to establish a carbon price for large emitters. Benchmarks were established at an industry sector level. For example, all in-situ operations would have their emissions measured and verified, and those with the lowest emissions per output would be used to set a High Performance Benchmark (HPB) emissions level. This best-in-class HPB would then be used to establish annual emission reduction targets for all operations/plants in that sector.

This made it easy for lower-emitting plants to comply and expensive for those with more emissions, which was the plan. It encouraged larger emitters to either invest in major changes at the plant or possibly shutter the emissions-heavy facility in favour of newer, cleaner operations.

Facilities that out-performed their emission reduction requirements could earn Emission Performance Credits (EPCs) which they could sell to others. Those unable to buy credits or otherwise meet the target could pay the regulated price of carbon to the province, which could use revenue to help big emitters invest in low-carbon changes.

2019

The UCP argued that the cost burden on larger emitters was too great and that it disadvantaged Alberta businesses compared to elsewhere in Canada (half true) and in the States (true). So, it changed TIER to lower the market price of carbon while leaving the regulated rate alone.

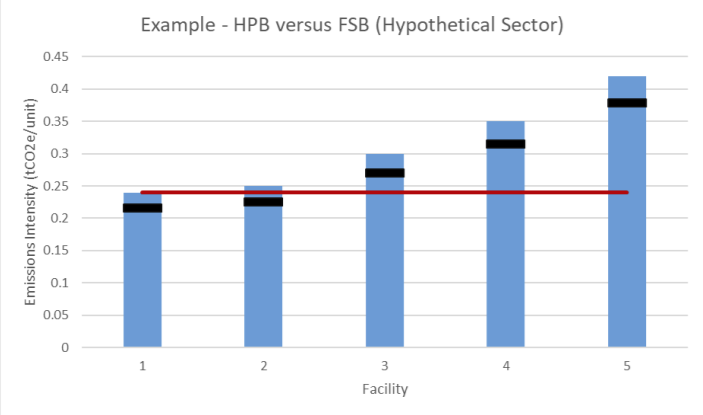

In 2019, operations no longer had to reduce emissions a percentage below the best-in-class HPB target for their sector. They only had to reduce their emissions based on the less stringent of the HPB or their own much higher emission levels. Of course, poor emission performers defaulted to facilities-based targets, dramatically reducing their compliance obligations.

Smaller compliance obligations meant less demand for EPCs and the increased credit supply lowered the market price of carbon.

2023

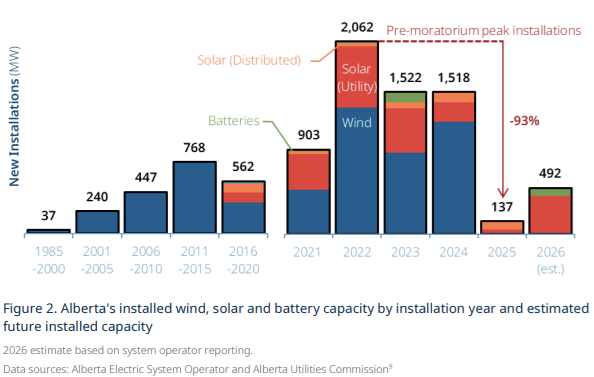

Compounding the over-supply was the renewable energy boom that hit Alberta in the early-2020s. Alberta is a largely open electricity market where developers can build generation of their choosing and sell the power to the grid. It is the only electricity market like this in Canada.

Alberta allowed renewables to earn credits for any output below an HPB based on gas generation which made the economics for renewables even more favourable, and the province became Canada’s epicentre of renewable energy growth. Roughly 6 GWs (gigawatts) of new wind and solar joined the market in just a few years adding huge volumes of EPCs to the market.

The UCP attempted to rein this in by limiting the crediting and validity periods of EPCs generated. However, the sheer volume of new credits kept the market value of EPCs at about $20-$40 even while the regulated price of carbon climbed much higher.

2025

Enter Smith’s UCP government, which adopted two new rules in late-2025 that drove the market price down to just $17/tonne. These included a pathway to earn EPCs for investments in low-carbon tech, regardless of whether emissions were lowered, and the right to reactivate recently used EPCs and use them again.

The market price likely would have tumbled further if Alberta hadn’t signed the MOU with the Feds indicating that pricing may be forced up.

TIER fixes

The regulated carbon price will climb to $130/tonne by 2030. Alberta and the Feds have lots of levers to boost the market price along with it. An easy first step would be to undo Smith’s late-2025 changes. No rational operator has made investment decisions based on those rules yet (the regulations aren’t even published), so there would be very limited economic fallout.

They could also move back to a sector-based HPB and drop the facility-specific compliance option. The renewable energy-based EPC oversupply could ease the transition in the near-term.

It could be enough to make these changes and monitor the impact through 2030, as no party wants to boost the market price all the way up to $130/tonne before then. Really, the market price should never fully reach the regulated value.

Sometime in the 2030s, the renewable energy credit glut may take care of itself as Alberta has dramatically tightened approval and costing of renewable energy projects and new installations have fallen. As HPBs tighten annually, emission-free electricity credits will decline and compliance requirements in other sectors will climb creating new demand.

If these measures are forecast to be insufficient after 2030, the Feds could take more direct action. For example, the EU established a carbon pricing system in the early 2000s and soon faced a nearly catastrophic surplus of allowances. It established the Market Stability Reserve (MSR), which removed allowances from the market when the surplus exceeded a pre-determined threshold to steady carbon prices.

In Alberta, the Feds could buy EPCs at a pre-determined rate at a volume needed to stabilize the market price closer to the regulated value.

Will Alberta agree?

The Feds aren’t empty-handed in the negotiations. The Supreme Court upheld the federal government’s right to regulate emissions, which Alberta avoids only by maintaining a comparably stringent TIER. Alberta also wants federal support for its data centre dreams that would be available under the MOU with a carbon price deal.

But, Alberta has intractably resisted a meaningful market carbon price and the Feds’ attempts to regulate it, and the province is prepping for a separation referendum so may not be in a compromising mood.